Monday–Friday · 9:00 AM – 5:00 PM ET·Florida-born · Insuring businesses nationwide

Coverage comparisons

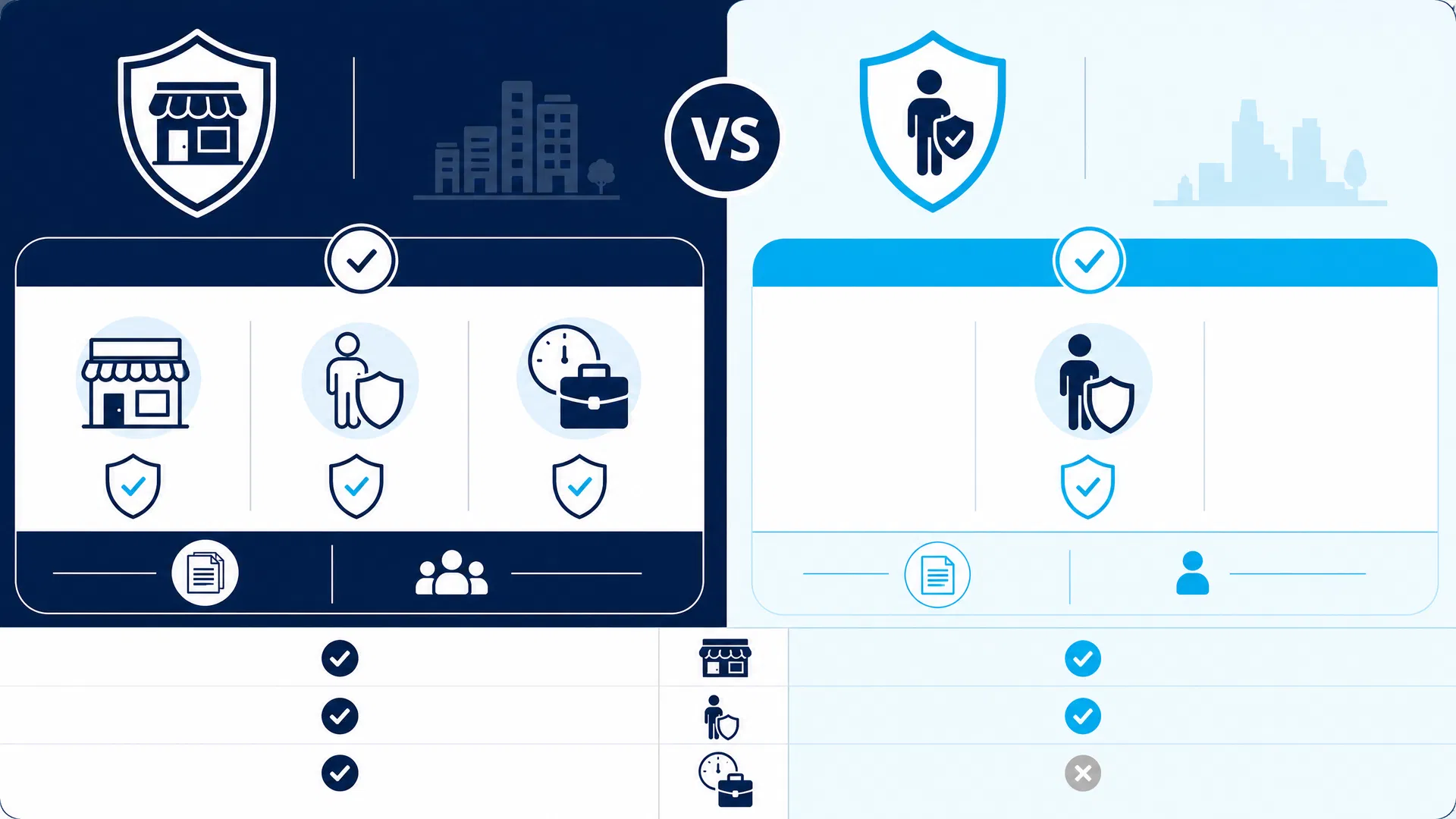

BOP vs General Liability Insurance: What Is the Difference?

Understand the difference between BOP vs General Liability insurance. Ellie Insurance Group helps businesses shop on your behalf for the right coverage.

Licensed Business Insurance Agent

Last reviewed June 2026 6 min read

Key takeaway

The primary difference between BOP vs General Liability insurance lies in their scope: General Liability (GL) covers third-party bodily injury and property damage, while a Business Owners Policy (BOP) bundles GL with.

Quick Answer

The primary difference between BOP vs General Liability insurance lies in their scope: General Liability (GL) covers third-party bodily injury and property damage, while a Business Owners Policy (BOP) bundles GL with commercial property and business interruption insurance into a single, cost-effective package. A BOP is often ideal for small to medium-sized businesses with physical assets, offering broader protection against common risks in one policy.

What Business Owners Need to Know

Navigating the world of commercial insurance can be complex, with various policies designed to protect different aspects of your business. Two terms that often cause confusion are Business Owners Policy (BOP) and General Liability (GL) insurance. While both are crucial for safeguarding your business, understanding the fundamental difference between BOP vs General Liability is key to securing the right coverage. Many business owners mistakenly believe one covers all their needs, leading to potential gaps in protection.

Ellie Insurance Group, founded in 2022, is Florida-born, insuring businesses nationwide. Our agents shop 100+ carrier markets on your behalf, ensuring you get the best rates and the right coverage for your unique business needs in Tampa and Brooksville, FL, and beyond.

General Liability Insurance: The Foundation

General Liability insurance is often considered the bedrock of a business insurance program. It protects your business from claims of third-party bodily injury, property damage, and personal and advertising injury (e.g., libel, slander). This coverage is essential for virtually any business, regardless of size or industry, as accidents can happen anywhere—on your premises, at a client's location, or even through your advertising efforts.

What General Liability Covers:

- Bodily Injury: If a customer slips and falls in your store and gets injured, GL can cover their medical expenses and legal fees if they sue.

- Property Damage: If your employee accidentally damages a client's property while working, GL can cover the repair or replacement costs.

- Personal and Advertising Injury: Covers claims of libel, slander, copyright infringement in your advertising, or wrongful eviction.

Business Owners Policy (BOP): The Bundle

A Business Owners Policy (BOP) is a comprehensive package designed for small to medium-sized businesses. It intelligently combines three critical coverages into one policy:

- General Liability Insurance: As described above, protecting against third-party claims.

- Commercial Property Insurance: Covers your business's physical assets, including your building (if you own it), equipment, inventory, furniture, and other business personal property, against perils like fire, theft, and vandalism.

- Business Interruption Insurance (also known as Business Income): This coverage helps replace lost income and cover ongoing operating expenses if your business has to temporarily close due to a covered property loss (e.g., a fire forces you to shut down for repairs).

Coverage Details and Common Mistakes

Choosing between a standalone GL policy and a BOP depends on your business's specific needs and risk profile. Here's a deeper dive into their differences and common misconceptions:

When to Choose a BOP

A BOP is generally recommended for businesses that:

- Have a physical location: Whether owned or leased, a BOP protects your premises and its contents.

- Possess physical assets: Inventory, equipment, computers, and furniture are covered.

- Are susceptible to business interruptions: If a covered event could halt your operations and cause significant financial loss.

- Meet eligibility requirements: Insurers typically have criteria for BOP eligibility, often based on business size, revenue, and industry risk. High-risk businesses or those with very complex operations may not qualify for a BOP and might need separate, customized policies.

When a Standalone General Liability Policy May Be Sufficient

A standalone GL policy might be more appropriate for businesses that:

- Don't have significant physical assets: For example, a home-based consultant with minimal equipment.

- Operate primarily remotely or virtually: Businesses with no physical office or inventory might not need property coverage.

- Are very small or new: Sometimes, a GL policy is a starting point before expanding to a BOP.

- Don't qualify for a BOP: Due to industry risk or size, some businesses must purchase separate policies.

Common Mistakes

- Assuming GL is Enough: Many business owners think General Liability covers everything. It does not cover your own property, lost income, or specialized risks like professional errors or cyberattacks.

- Overlooking Business Interruption: This is a critical component of a BOP that many businesses underestimate. Without it, a fire or other disaster could lead to permanent closure.

- Not Reviewing Eligibility: As your business grows or changes, you might outgrow your BOP eligibility or find that a BOP no longer provides adequate coverage for your evolving risks.

How This Applies in Florida and Licensed States

In Florida, like many other states, the availability and structure of BOPs and General Liability policies are standard, but local factors can influence specific coverages and rates.

Florida-Specific Considerations

- Property Risks: Florida businesses face unique property risks, particularly from hurricanes, tropical storms, and associated wind and flood damage. While a BOP covers many property perils, it typically excludes flood damage and may have specific deductibles or exclusions for windstorm coverage. Businesses in Florida often need to supplement their BOP with separate commercial flood insurance and ensure their wind coverage is adequate.

- Business Interruption: Given the potential for severe weather events to cause prolonged business closures, robust business interruption coverage within a BOP is particularly vital for Florida businesses.

Ellie Insurance Group, Florida-born, insuring businesses nationwide, understands these regional nuances. We help businesses in Tampa, Brooksville, and across our licensed states tailor their insurance portfolios to address both common and localized risks.

When to Review Your Policy

Your business is dynamic, and your insurance should be too. Regularly reviewing your policies ensures they continue to meet your needs.

Triggers for Review

- Business Growth or Expansion: Adding new locations, increasing inventory, or hiring more employees can change your property and liability exposures.

- Changes in Operations: Introducing new services, products, or processes might require different types of coverage or adjustments to your existing policies.

- Relocation: Moving to a new premises can significantly impact your property insurance needs and local liability risks.

- Annual Renewal: Always take the opportunity at renewal time to discuss your current business operations and any changes with your agent.

Related Commercial Insurance Pages

FAQs

Is a Business Owners Policy required by law?

No, a Business Owners Policy (BOP) is not legally required. However, many businesses choose to purchase it because it provides comprehensive protection against common risks, and landlords or clients may require you to carry certain coverages included in a BOP.

Can I get General Liability insurance without a BOP?

Yes, you can purchase a standalone General Liability insurance policy. This is often suitable for businesses that don't have significant physical assets or a physical location, or for those that don't qualify for a BOP due to their industry or size.

Does a BOP cover professional mistakes?

No, a standard BOP does not cover professional mistakes or negligence. For that, you would need a separate Professional Liability (Errors & Omissions) insurance policy, which is crucial for businesses that provide advice or services.

What is business interruption insurance, and why is it important?

Business interruption insurance, included in a BOP, helps replace lost income and cover ongoing operating expenses if your business has to temporarily close due to a covered property loss, such as a fire or severe storm. It's vital for ensuring your business can recover financially after a disruption.

How does Ellie Insurance Group help with BOP and General Liability?

Ellie Insurance Group helps business owners understand the differences between BOP and General Liability, assessing their unique risks to recommend the most suitable coverage. We shop 100+ carrier markets to find the best rates and comprehensive protection for your business.

Instant Quote

Ready to secure comprehensive protection for your business? Understand the difference between BOP and General Liability and get the coverage that fits your needs. Let Ellie Insurance Group shop on your behalf for the best rates. Get your Instant Quote today and safeguard your business against unforeseen risks.

Working with an independent agent

Coverage needs vary by operation, contract, and state. An Ellie Insurance Group agent can review your situation and shop 100++ carrier markets on your behalf — start an Instant Quote or call 813-582-5215.

Get a real quote

Want a quote for the coverage discussed here? Start with general liability, workers' compensation, or commercial auto — or browse all commercial coverages and industries we serve.

Written & reviewed by

Licensed Business Insurance Agent · Ellie Insurance Group

Licensed business insurance agent at Ellie Insurance Group · Access to 100+ carrier markets.

More about KevinIndependent Agency

100+ carrier markets

5.0★ Google Rating

Verified Google reviews

Trusted Choice 5.0

5-star independent agency

InsuredBetter 5.0

29 verified client reviews

Same-Day Certificates

For active clients during business hours

Instant Commercial Quotes

Most submissions, same business day

Keep reading

Related Articles

Coverage comparisons

Additional Insured vs Certificate Holder: What Business Owners Should Know

An additional insured is an entity added to another's insurance policy, gaining direct coverage and protection under that policy, often required by contract [3]. A certificate holder, conversely, merely receives a…

Coverage comparisons

General Liability vs Professional Liability Insurance

General Liability (GL) insurance primarily covers third-party bodily injury and property damage claims arising from your business operations, premises, or products. Professional Liability insurance, also known as Errors…

Compliance & renewals

7 Certificate of Insurance Mistakes That Get Contractors Booted Off Jobs

Most certificate of insurance (COI) rejections come from a short list of fixable errors — blanket additional insured wording where a specific named endorsement is required, a missing waiver of subrogation, no primary…

Next step

Ready to shop commercial coverage?

Talk to a commercial agent or run an instant quote online — same-day binding on most commercial submissions during business hours.