Monday–Friday · 9:00 AM – 5:00 PM ET·Florida-born · Insuring businesses nationwide

Coverage comparisons

Additional Insured vs Certificate Holder: What Business Owners Should Know

Understand the crucial differences between additional insured and certificate holder statuses, endorsements, COIs, and common mistakes to protect your business. Ellie Insurance Group helps Florida businesses navigate complex insurance needs.

Licensed Business Insurance Agent

Last reviewed June 2026 8 min read

Key takeaway

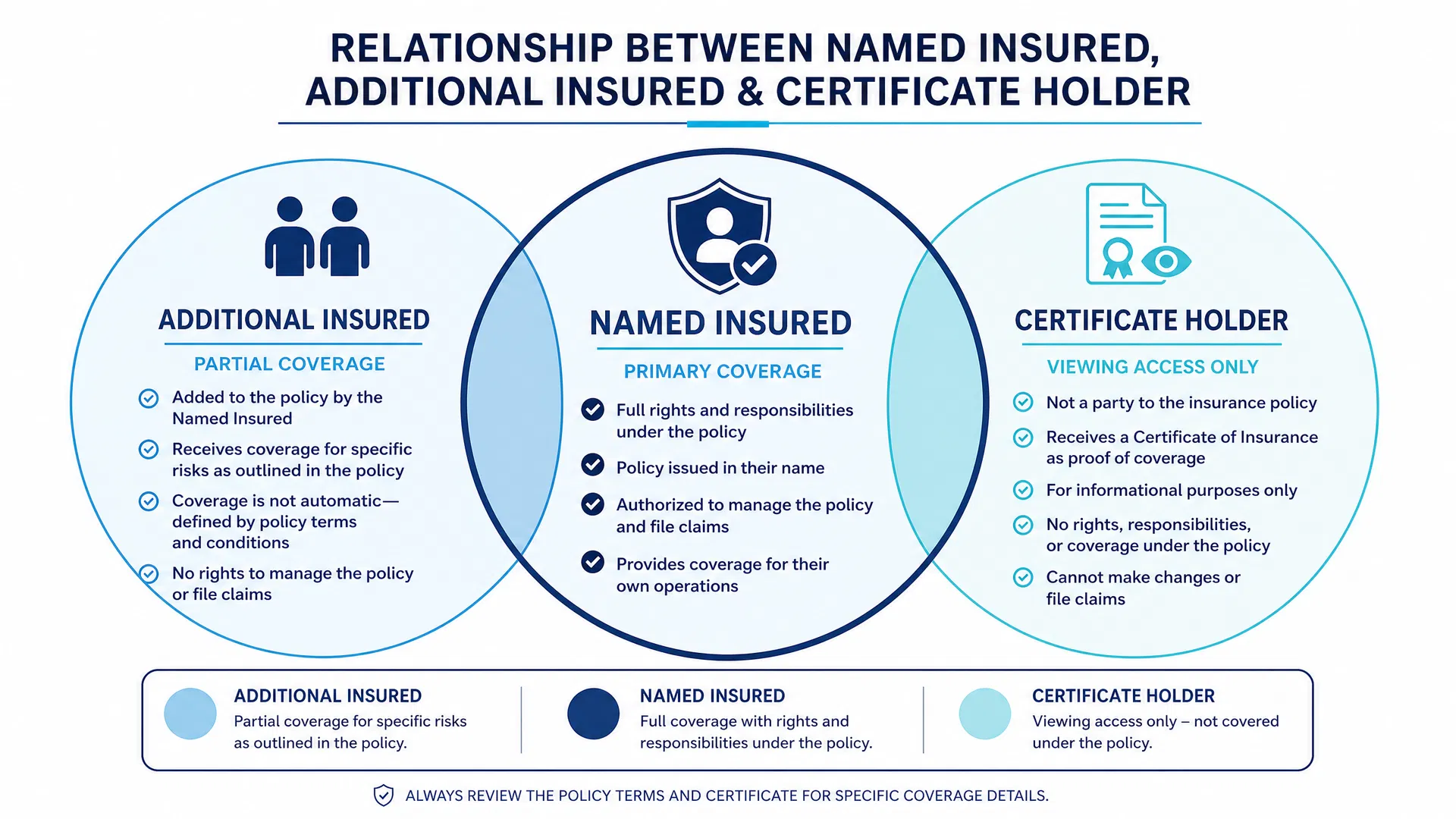

An additional insured is an entity added to another's insurance policy, gaining direct coverage and protection under that policy, often required by contract [3].

Quick Answer

An additional insured is an entity added to another's insurance policy, gaining direct coverage and protection under that policy, often required by contract [3]. A certificate holder, conversely, merely receives a Certificate of Insurance (COI) as proof that a policy exists, without receiving any direct coverage [4].

Understanding the distinction between an additional insured vs certificate holder is crucial for business owners navigating contracts and liability. This knowledge helps ensure proper protection for your business and its partners. For comprehensive general liability coverage tailored to your needs, visit our General Liability page. Understanding these distinctions is not just about compliance; it's about strategic risk management. Many business owners, especially those new to commercial contracts, often overlook the critical differences, assuming a Certificate of Insurance (COI) provides the same protection as being an additional insured. This misconception can lead to significant financial exposure if a claim arises. Our agents are here to clarify these complexities and ensure your business is adequately protected. To learn more about how general liability can protect your business, Instant Quote.

What Business Owners Need to Know

In the world of business contracts and risk management, the terms additional insured and certificate holder are frequently encountered, yet their implications are vastly different. Misinterpreting these roles can lead to significant gaps in coverage or unexpected liabilities. Ellie Insurance Group, founded in 2022 in Tampa and Brooksville, FL, helps business owners clarify these critical distinctions.

An additional insured is a person or organization, other than the named insured, who is protected by an insurance policy. This status is typically granted via an endorsement to the original policy and is often a contractual requirement [3]. For example, a general contractor might require a subcontractor to name them as an additional insured on the subcontractor's general liability policy. This means if a claim arises from the subcontractor's work, the general contractor could be covered under the subcontractor's policy, providing an extra layer of protection. This arrangement is a cornerstone of effective risk transfer in many industries, particularly construction, real estate, and event management. It ensures that the party requiring the insurance has a direct line of defense through the primary policy, reducing their reliance on their own insurance in certain situations. Without this status, the requesting party would typically have to rely on their own insurance, which could lead to higher deductibles and potentially impact their claims history. The specific wording of the additional insured endorsement is crucial, as it defines the scope and limits of the coverage extended to the additional insured. Our agents can help you review these endorsements to ensure they meet your contractual obligations and provide the protection you expect.

Conversely, a certificate holder is simply the recipient of a Certificate of Insurance (COI). A COI is a document that summarizes the key aspects of an insurance policy, such as coverage types, limits, and policy effective dates [4]. It serves as proof that an insured party has a policy in place but does not confer any direct coverage to the certificate holder. A landlord, for instance, might request a COI from a tenant to verify they have liability insurance, but the landlord is not covered by that policy unless they are also named as an additional insured. It's important to note that a COI is merely a snapshot of the policy at the time it's issued and does not guarantee future coverage or policy terms. It's a common administrative tool used for verification, but it should never be confused with an actual insurance policy or an endorsement that grants coverage. Businesses often exchange COIs to demonstrate compliance with contractual insurance requirements, but relying solely on a COI for protection is a significant risk. Our agents can guide you through the process of requesting and understanding COIs, ensuring you have accurate documentation without misinterpreting its legal implications.

Endorsements and Contracts

Becoming an additional insured almost always requires a specific endorsement to the original insurance policy. This endorsement modifies the policy to extend coverage to the newly added party. The scope of this coverage can vary significantly depending on the endorsement's wording, so it's vital to review it carefully. Contracts often stipulate the need for additional insured status to transfer risk from one party to another.

Without an endorsement, a COI alone is insufficient to grant additional insured status. The COI merely reflects the policy's status at a given time and is not the policy itself [4]. Relying solely on a COI for protection when additional insured status is needed is a common and potentially costly mistake. This is why it's crucial to work with an experienced agent who can guide you through the process of obtaining the correct endorsements and verifying that your contracts are properly fulfilled. For more information on how general liability can protect your business, Instant Quote.

Coverage Details and Common Mistakes

The nuances between these two statuses can be complex, leading to several common pitfalls for business owners. Ellie Insurance Group shop on your behalf across 100+ carriers for the best rates, ensuring you get the right coverage without these common errors. Our Florida-born agency is dedicated to helping businesses nationwide navigate these complexities and secure robust protection.

| Feature | Additional Insured | Certificate Holder |

|---|---|---|

| Coverage | Receives direct coverage under the policy | Receives no direct coverage |

| Protection | Protected against claims arising from named insured's actions | Receives proof of insurance only |

| Requirement | Requires policy endorsement [3] | Requires only a Certificate of Insurance (COI) [4] |

| Purpose | Transfers risk, satisfies contractual obligations | Verifies existence of insurance |

| Cost | May incur additional premium for named insured | No cost to the certificate holder |

Common Mistakes:

- Assuming COI grants coverage: Many business owners mistakenly believe that receiving a COI means they are covered by the policy. This is incorrect; a COI is informational only [4].

- Vague contractual language: Contracts that vaguely request "proof of insurance" without specifying "additional insured" status can leave parties unprotected.

- Not reviewing endorsements: The specific language of an additional insured endorsement dictates the scope of coverage. Failing to review this can lead to inadequate protection.

- Outdated COIs: Insurance policies renew annually. An outdated COI might not reflect current coverage or policy status.

How This Applies in Florida and Licensed States

For businesses operating in Florida, understanding these distinctions is particularly important due to the state's dynamic business environment. Ellie Insurance Group is Florida-born, insuring businesses nationwide, and our agents are well-versed in the specific requirements and common practices in Florida, including our local communities of Tampa and Brooksville, FL.

While the core definitions of additional insured and certificate holder are universal, how they are applied can vary based on state regulations and industry-specific contracts. For example, certain construction contracts in Florida might have specific requirements for additional insured endorsements. It's crucial to remember that state requirements for business insurance can vary significantly [1].

Ellie Insurance Group helps businesses across Florida and other licensed states navigate these complexities. Our deep understanding of local and national insurance landscapes ensures that your business complies with contractual obligations and is adequately protected, whether you're a small startup or a growing enterprise. For more information on how we can help you secure the right coverage, an Instant Quote.

When to Review Your Policy

Regularly reviewing your insurance policies and contractual agreements is a best practice for all business owners. The U.S. Small Business Administration recommends reassessing your business insurance needs annually 1. This is especially true when:

- Entering new contracts: Each new contract might introduce different requirements for additional insured status or COIs.

- Changes in business operations: Expanding services, hiring new employees, or acquiring new assets can alter your risk profile.

- Policy renewal: This is an ideal time to ensure all endorsements and certificate holder arrangements are up-to-date.

- Significant events: Mergers, acquisitions, or major changes in business structure warrant a thorough review.

An Ellie Insurance Group agent can help you review your current policies and contracts to ensure you have the appropriate coverage and that all additional insured and certificate holder requirements are met. Instant Quote to ensure your business is fully protected.

Related Commercial Insurance Pages

- Commercial Auto Insurance

- Workers' Compensation Insurance

- Professional Liability Insurance

- Commercial Property Insurance

- Business Owner's Policy (BOP)

FAQs

Q: Can a certificate holder sue the insurance company?

A: No, a certificate holder generally cannot sue the insurance company directly for coverage under the policy. They are not a party to the insurance contract and receive no direct coverage. Their COI only proves that the named insured has a policy 4. Only an additional insured, as a party covered by endorsement, would typically have the standing to make a claim or sue for coverage.

Q: Is an additional insured always covered for everything?

A: Not necessarily. The scope of coverage for an additional insured is defined by the specific endorsement added to the policy. This endorsement might limit coverage to specific operations, locations, or types of claims. It's crucial to read the endorsement carefully to understand the exact extent of the protection 3.

Q: Why do clients ask to be named as additional insured?

A: Clients often ask to be named as an additional insured to protect themselves from liability arising from your work or services. This transfers some of the risk to your insurance policy, providing them with direct coverage if they are implicated in a claim related to your operations. It's a common risk management strategy in many industries.

Q: What is the difference between primary and non-contributory additional insured?

A: This refers to how an additional insured's policy interacts with other available insurance. "Primary" means the named insured's policy will pay first, without seeking contribution from the additional insured's own policies. "Non-contributory" means the named insured's policy will not seek contribution from the additional insured's policies. This wording provides maximum protection to the additional insured.

Q: How long does it take to get a Certificate of Insurance (COI)?

A: Typically, an agent can issue a Certificate of Insurance (COI) very quickly, often within minutes or a few hours, once the request is made and the policy information is verified. It's a standard administrative task for insurance providers.

Q: Does Ellie Insurance Group help with additional insured endorsements?

A: Yes, Ellie Insurance Group agents regularly assist business owners with obtaining and understanding additional insured endorsements. We work with our carriers to ensure your policies meet contractual requirements and provide the necessary protection for your business and its partners.

Instant Quote

Ready to secure the right insurance for your business and navigate complex contractual requirements with confidence? Ellie Insurance Group is here to help. We shop on your behalf across 100+ carriers to find the best rates and comprehensive coverage. Get your Instant Quote today and protect your business effectively.

References

Working with an independent agent

Coverage needs vary by operation, contract, and state. An Ellie Insurance Group agent can review your situation and shop 100++ carrier markets on your behalf — start an Instant Quote or call 813-582-5215.

Get a real quote

Want a quote for the coverage discussed here? Start with general liability, workers' compensation, or commercial auto — or browse all commercial coverages and industries we serve.

Written & reviewed by

Licensed Business Insurance Agent · Ellie Insurance Group

Licensed business insurance agent at Ellie Insurance Group · Access to 100+ carrier markets.

More about KevinIndependent Agency

100+ carrier markets

5.0★ Google Rating

Verified Google reviews

Trusted Choice 5.0

5-star independent agency

InsuredBetter 5.0

29 verified client reviews

Same-Day Certificates

For active clients during business hours

Instant Commercial Quotes

Most submissions, same business day

Keep reading

Related Articles

Coverage comparisons

General Liability vs Professional Liability Insurance

General Liability (GL) insurance primarily covers third-party bodily injury and property damage claims arising from your business operations, premises, or products. Professional Liability insurance, also known as Errors…

Coverage comparisons

BOP vs General Liability Insurance: What Is the Difference?

The primary difference between BOP vs General Liability insurance lies in their scope: General Liability (GL) covers third-party bodily injury and property damage, while a Business Owners Policy (BOP) bundles GL with…

Coverage explainers

Does General Liability Cover Property Damage?

Yes, general liability insurance typically covers third-party property damage that your business causes during its operations. However, it does not cover damage to your own business property, which requires a separate…

Next step

Ready to shop commercial coverage?

Talk to a commercial agent or run an instant quote online — same-day binding on most commercial submissions during business hours.